The Petty Cash Book (Cambridge (CIE) IGCSE Accounting): Revision Note

Syllabus Edition

First teaching 2021

Last exams 2026

Exam code: 0452 & 0985

The petty cash book

What is a petty cash book?

A petty cash book is used to record transactions involving small amounts of cash

The business will decide what they classify as small amounts of cash

Exam questions commonly tell you to class transactions for anything up to $100 or $75 as petty cash transactions

A petty cash voucher is used to record the transaction when money is taken from the petty cash account

It should state the amount and details

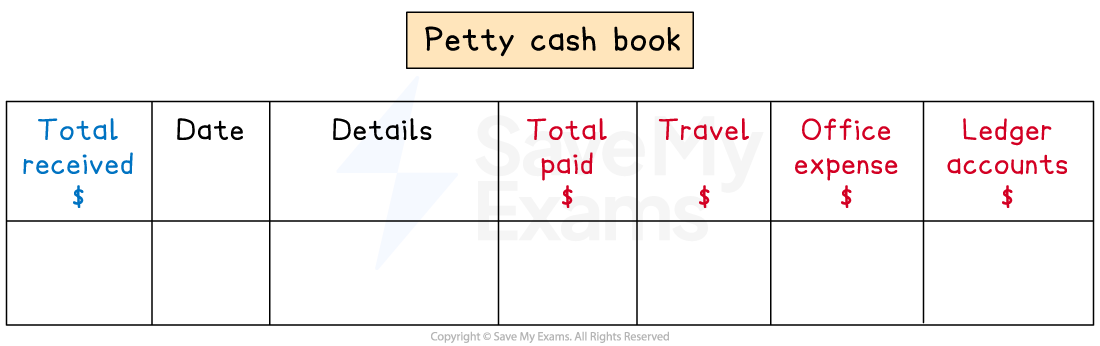

What is the layout of a petty cash book?

There is a date column and a details column

These commonly appear once in the middle

The total received column on the debit side states the total amount received for each transaction

The total paid column on the credit side states the total amount paid for each transaction

There are analysis columns on the credit side to separate payments into different categories

There are columns for the expense accounts and a column for the purchases ledger accounts

How do I enter transactions into the petty cash book?

The opening balance is on the debit side

The debit side shows the cash receipts

Small cash receipts from trade receivables

Money transferred from the cash or bank account to top up the petty cash account

The credit side shows the cash payments

Small cash payments for expenses

Small cash payments to trade payables

When you enter a transaction onto the credit side

You need to enter it in the appropriate analysis column(s)

Put the total for that transaction in the total paid column

How do I balance the petty cash book?

Find the total for each column on the credit side

Underline the totals for the analysis columns

These balances then get transferred to the relevant ledger accounts

You can transfer the total for each expense column rather than transfer each transaction separately

The entries for ledger accounts will need to be entered into the individual ledger accounts

Find the difference between the total paid and the total received

Put this entry as balance c/d on the side with the smaller total

This will usually be the credit side

Complete the balancing process for these two columns

Find the totals for the total received and total paid columns

Bring down the balance to the start of the next month

The balance brought down will always be on the debit side

Worked Example

Nazim is a sole trader. Nazim makes all payments of less than $75 by petty cash. Nazim ensures that there is exactly $150 in the petty cash account at the start of each month.

Below are the cash transactions for January 2024.

January 5 | Paid taxi fare, $23 |

8 | Paid cash, $45, to Jamie, a trade payable |

13 | Paid $25 for stationery |

17 | Received cash, $67, from Hawa, a trade receivable |

25 | Paid train fare, $51 |

30 | Paid cash, $17, to Melody, a trade payable |

Enter these transactions into Nazim’s petty cash book. Balance the account and bring down the balance on 1 February 2024.

Total Received $ | Date | Details | Total Paid $ | Travel $ | Office expenses $ | Ledger accounts $ |

150 | 2024 |

Balance b/d |

Answer:

Total received

$150 + $67 = $217

Total paid

$23 + $45 + $25 + $51 + $17 = $161

Find the difference

$217 - $161 = $56

Total Received $ | Date | Details | Total Paid $ | Travel $ | Office expenses $ | Ledger accounts $ |

150 | 2024 |

Balance b/d | ||||

Jan 5 | Taxi fare | 23 | 23 | |||

Jan 8 | Jamie | 45 | 45 | |||

Jan 13 | Stationery | 25 | 25 | |||

67 | Jan 17 | Hawa | ||||

Jan 25 | Train fare | 51 | 51 | |||

Jan 30 | Melody | 17 |

|

| 17 | |

161 | 74 | 25 | 62 | |||

| Jan 31 | Balance c/d | 56 | |||

217 | 217 | |||||

56 | Feb 1 | Balance b/d |

The imprest system

What is the imprest system?

The imprest system is used by businesses to ensure that the money in the petty cash account is equal to a set amount

This amount is known as the imprest amount

This is usually done at the start of each week or month

If the petty cash account is less than the imprest amount at the start of a period

Then it will be topped up using the cash or bank account

If the petty cash account is higher than the imprest amount at the start of a period

Then the excess can be deposited into the cash or bank account

The imprest amount will always be equal to:

The current balance of the petty cash account

Plus the total value of petty cash vouchers for the current period

Minus the total amount of petty cash received

What are the advantages of using an imprest system?

It sets a limit on the amount of cash which can be spent

It helps managers monitor the amount of petty cash that is being spent

It limits the amount of cash that could be mislaid or stolen

Examiner Tips and Tricks

Read the question carefully to see whether you are asked to restore the imprest or not. Also, check when the imprest is restored.

Worked Example

Mark maintains a petty cash account using the imprest system. The imprest amount, $200, is restored on the first day of every month.

During January 2024, Mark receives $50 from trade receivables, and the total of the petty cash vouchers for payments is $120.

Calculate how much cash is needed to restore the imprest on 1 February 2024.

Answer:

Find the net amount that left the petty cash account

$120 - $50 = $70

$70 is needed to restore the imprest

Unlock more, it's free!

Join the 100,000+ Students that ❤️ Save My Exams

the (exam) results speak for themselves:

Was this revision note helpful?