Statement of Financial Position (Balance Sheet) (DP IB Business Management) : Revision Note

The Statement of Financial Position

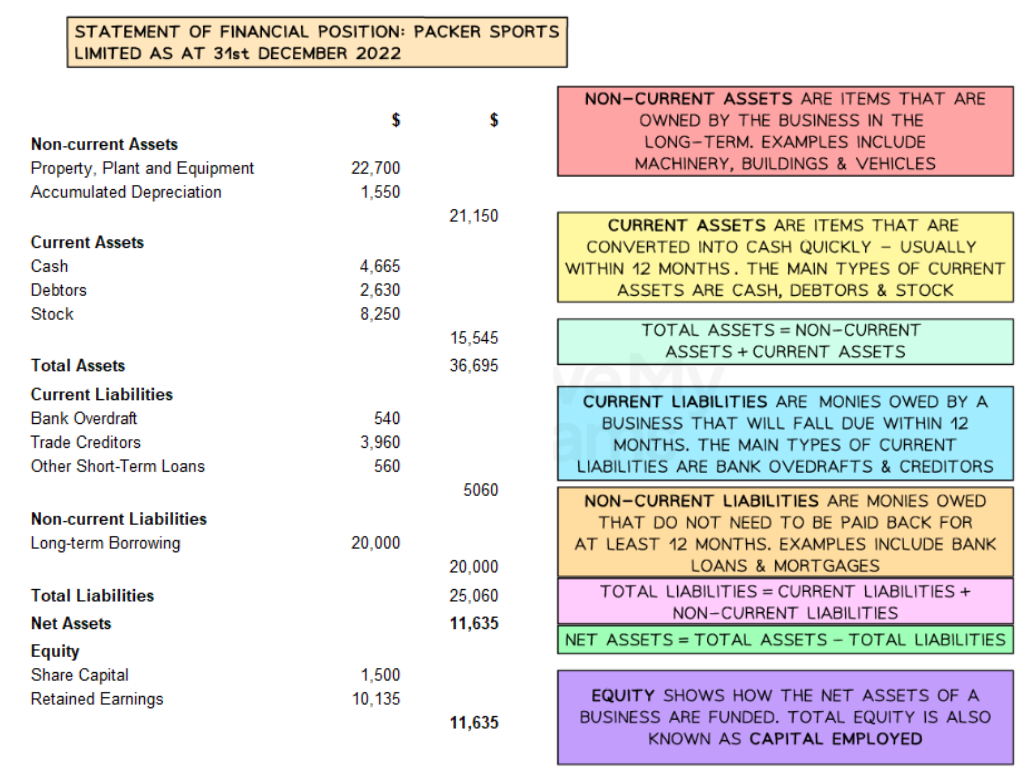

The Statement of Financial Position shows the financial structure of a business at a specific point in time

It identifies a businesses assets and liabilities and specifies the capital (equity) used to fund the business

The Statement of Financial Position is also known as the Balance Sheet

It is called the balance sheet, as net assets should equal the total equity

Diagram: the statement of financial position

Calculating the total assets

On the stated date Packer Sports Ltd owned non-current assets worth $24,250

It owns property, plant and machinery that is valued at $22,700

These assets have been depreciated by $1,550

The value of its current assets was $15,545, comprised of cash, debtors and stock

Total assets were therefore

![]()

Calculating total liabilities

On the stated date Packer Sports Ltd had current liabilities worth $5,060, comprised of a bank overdraft, trade creditors and other short-term loans

The value of its long-term liabilities were $20,000

Total liabilities were therefore

![]()

Calculating the net assets

Packer Sports Limited's net assets were therefore

![]()

Calculating total equity

Net assets of $14,735 were funded through share capital of $1,500 and retained earnings of $13,235

Examiner Tips and Tricks

In Paper 2 you may be asked to construct a balance sheet from given data.

To achieve full marks you must follow the format illustrated above and you should check that you have

Included all of the relevant headings in the correct order

Non-current assets

Current assets

Total assets

Current liabilities

Non-current liabilities

Total liabilities

Net assets

Equity

Correctly classified items under each heading

For example, you need to ensure that you have correctly allocated cash, stock and debtors as current assets, and creditors and bank overdrafts as current liabilities

Omitted irrelevant figures that belong to the profit and loss account

For example, costs and revenues are not included in the balance sheet

How Stakeholders use the Statement of Financial Position

Stakeholders will use the Statement of Financial Position alongside the Statement of Profit or Loss to perform ratio analysis and compare performance over time or with other businesses

How Stakeholders use the Statement of Financial Position

Stakeholder | Interest in the Balance Sheet |

|---|---|

Shareholders |

|

Managers & Directors |

|

Suppliers and Creditors |

|

Employees |

|

Examiner Tips and Tricks

Information found in the Statement of Profit or Loss and Statement of Financial Position can be used in a range of answers.

For example, if you are answering a question about sources of finance you might be able to use the capital structure of the business to recommend whether a business should borrow or look at an alternative source.

If a business already relies heavily on borrowing, it may be more sensible to recommend seeking to raise more share capital.

Different types of Intangible Assets

Intangible assets are non-physical assets that cannot physically be held but hold value for a business

Businesses need to account for intangible assets in their annual reports as it adds to the value of the business

Diagram: intangible assets

Intellectual property

This includes patents, trademarks, patents and copyrights which protect unique ideas, inventions, artistic works, and brand names

Brand value

The reputation and recognition associated with a brand has a value

It includes the brand name, logo, slogans, and customer loyalty to the brand

Customer relationships

Long-term relationships with customers including customer lists, contracts, and customer loyalty programs

These relationships can provide recurring revenue and a competitive advantage

Software and technology

Proprietary software, computer programs and technology systems that are crucial to a business's operations or provide a competitive advantage

Contracts and agreements

Long-term contracts, lease agreements, licensing agreements and franchise agreements that have value and contribute to future cash flows

Agreements with employees or business partners that restrict them from competing with the company for a specific period which protect the company's interests and market position (non compete contract)

Goodwill

The value of a company's reputation, customer base and brand

Goodwill often represents the premium paid when one business takes over or merges with another business

Domain names and other online assets

Valuable domain names, websites, social media accounts and online platforms that drive customer engagement, traffic, and online presence

Licenses and permits

Licenses, permits, and regulatory approvals that grant exclusive rights or access to certain markets or resources, often issued by governments

You've read 0 of your 5 free revision notes this week

Sign up now. It’s free!

Did this page help you?