Characteristics of Aggregate Supply (Edexcel A Level Economics A): Revision Note

Exam code: 9EC0

The Aggregate Supply (AS) Curve

Aggregate supply is the total supply of goods/services produced within an economy at a specific price level at a given time

The SRAS curve is upward sloping due to two reasons

The aggregate supply is the combined supply of all individual supply curves in an economy which are also upward sloping

As real output increases, firms have to spend more to increase production e.g. wage bills will increase

Increased costs result in higher average prices

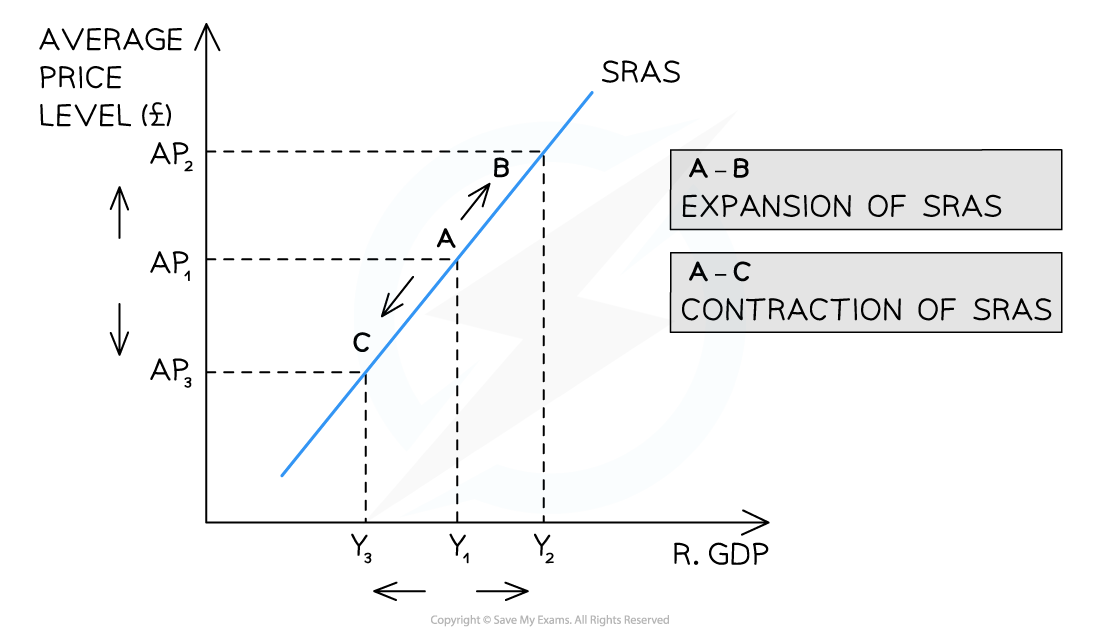

A movement along the SRAS curve

Whenever there is a change in the average price level (AP) in an economy, there is a movement along the short run aggregate supply (SRAS) curve

Diagram analysis

An increase in the AP (ceteris paribus) from AP1 → AP2 leads to a movement along the SRAS curve from A → B

There is an expansion (extension) of real GDP from Y1 → Y2

A decrease in the AP (ceteris paribus) from AP1 → AP3 leads to a movement along the SRAS curve from A → C

There is a contraction of real GDP (output) from Y1→Y3

A shift of the entire SRAS curve

Whenever there is a change in the conditions of supply in an economy (e.g. costs of production), there is a shift of the entire SRAS curve

Diagram analysis

A decrease in labour costs results in a shift right of the entire curve from SRAS1 → SRAS2

At every price level, output and real GDP have increased from Y1 → Y2

An increase in labour costs results in a shift left of the entire curve from SRAS1 → SRAS3

At every price level, output and real GDP have decreased from Y1 → Y3

The Relationship Between Short-run & Long-run AS

Short run aggregate supply (SRAS) is influenced by changes in the costs of production

Short run refers to the time period where at least one factor of production is fixed

Long run aggregate supply (LRAS) is influenced by a change in the productive capacity of the economy

Productive capacity is changed by changes to the quantity or quality of the factors of production

When production capacity changes, it is equivalent to a shift inwards/outwards of the production possibilities frontier (PPF)

Long term economic growth requires the productive capacity to increase

Unlock more, it's free!

Did this page help you?