Stock Control (Edexcel A Level Business) : Revision Note

Interpretation of stock control diagrams

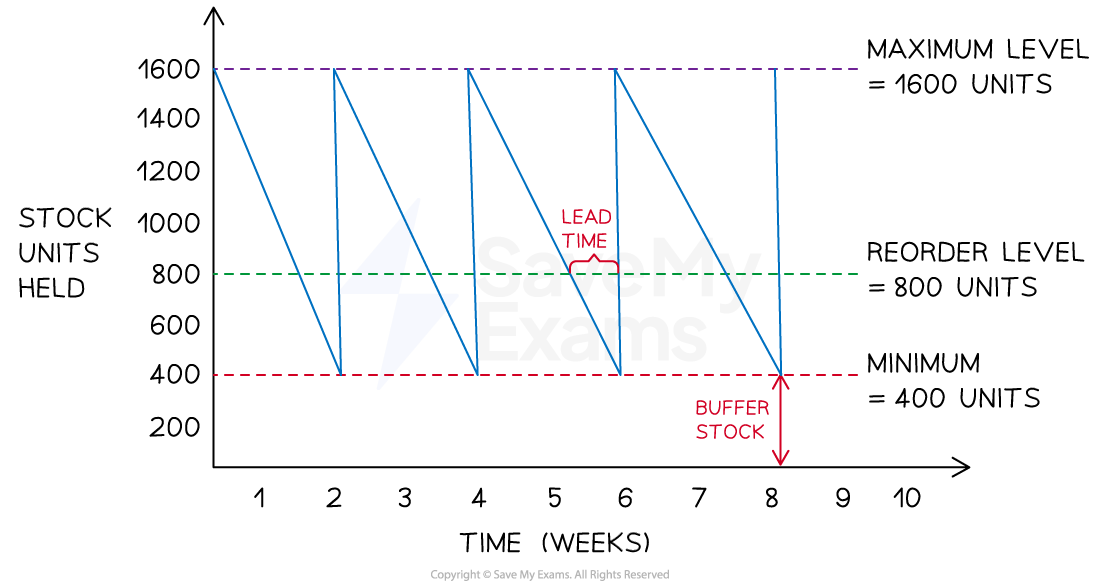

A stock control diagram illustrates the flow of stock (inventory) into and out of a business over time

Example stock control diagram

Diagram analysis

The maximum stock level is the maximum amount of stock a business is able to hold in normal circumstances (1600)

The reorder level is the level at which a business places a new order with its supplier (800)

The minimum stock level is also known as the buffer stock level and is the lowest level to which a business is willing to allow stock levels to fall (400)

The lead time is the length of time from the point of stock being ordered from the supplier to it being delivered (1 week)

The stock level line shows how stock levels change over the given time period

As stock is used up a downwards slope is plotted

When an order is delivered by a supplier the stock level line shoots upwards

Worked Example

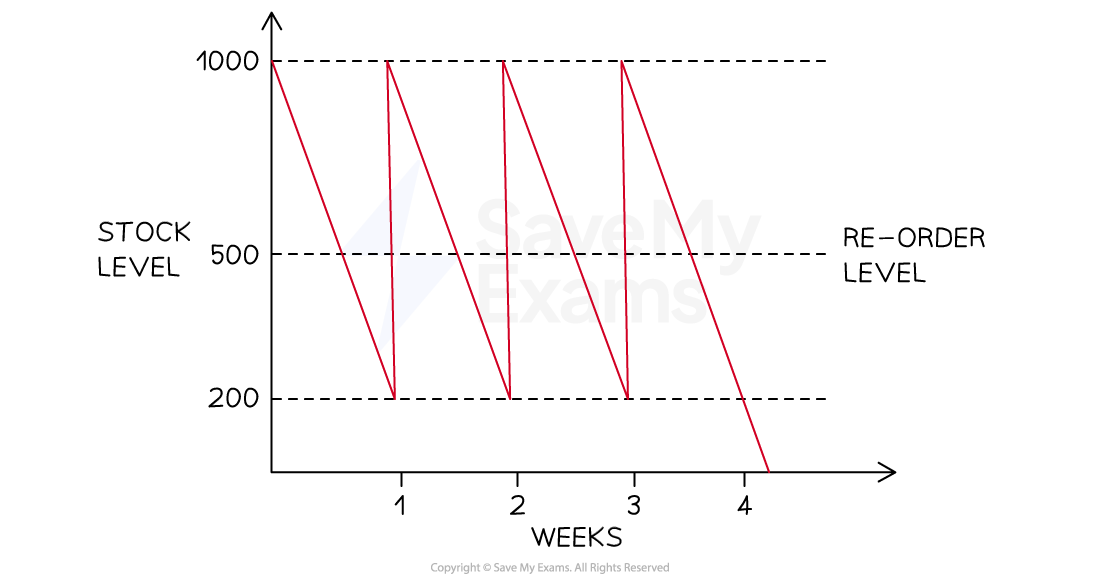

The diagram below shows stock movements of kitchen shelving units sold by TamFix Ltd.

Identify the following points:

the minimum stock level

the re-order level

the re-order quantity

the lead time for kitchen shelving units (4)

Step 1 - Identify the minimum stock level

The minimum stock level is identified by the bottom-most dotted line - in this case it shows that the minimum stock level is 200 units (1)

Step 2 - Identify the reorder level

The reorder level is clearly identified on the diagram - in this case it shows that the reorder level is 500 units (1)

Step 3 - Identify the reorder quantity

The reorder quantity is the difference between the maximum stock level (shown by the topmost dotted line) and the minimum stock level

1000 units (maximum stock) - 200 units (minimum stock) = 800 units

The reorder quantity is therefore 800 units (1)

Step 4 - Identify the lead time for kitchen shelving units

The lead time is the difference in time between an order for stock being placed and its delivery. In this case, assuming a five-day working week, the lead time for shelving units is two days (1)

Buffer stock

Buffer stock is a quantity of goods/raw materials kept in case of stock shortages

This can provide a competitive edge over rivals unable to meet demand

This approach is commonly called ‘just in case’ stock control

The decision to keep buffer stocks is one that businesses have to weigh up very carefully

The decision will be influenced by the nature of the business and the product/service it provides

Advantages and disadvantages of holding buffer stock

Advantages | Disadvantages |

|---|---|

|

|

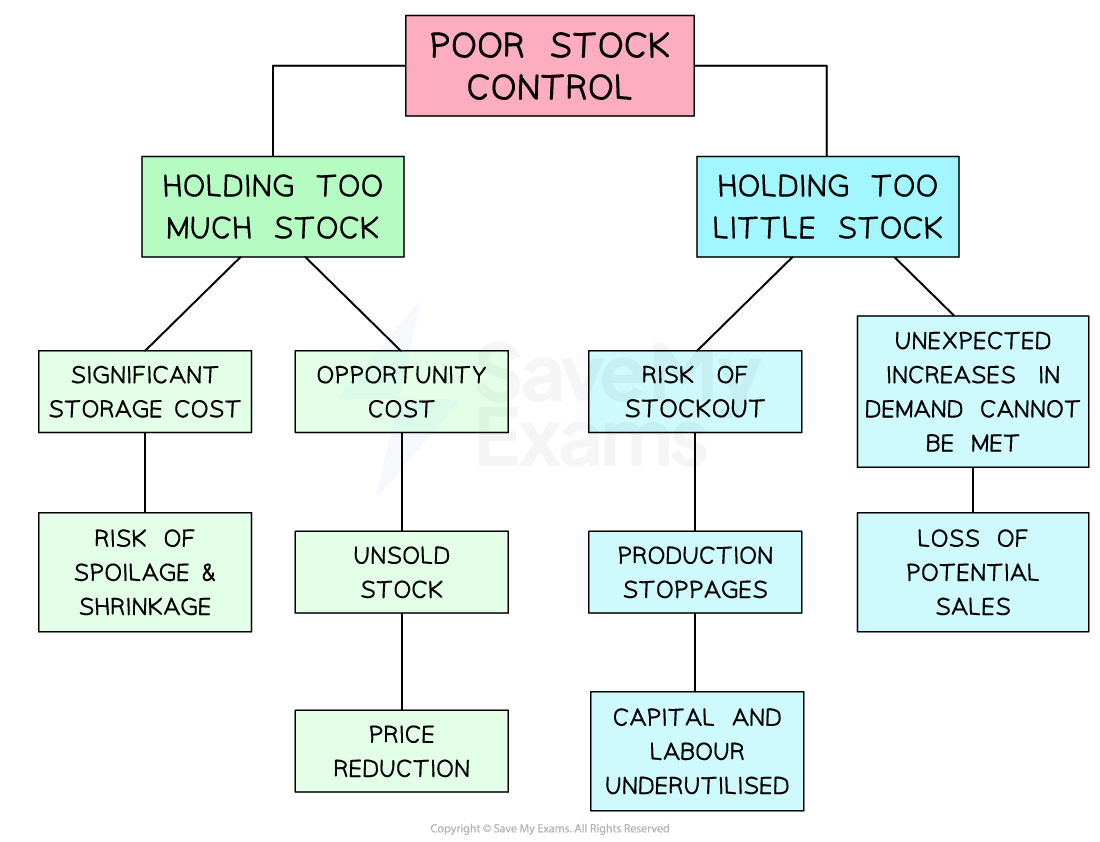

Implications of poor stock control

Too much or too little stock: implications

Problems may arise from holding too much stock

Storage costs (e.g. warehouse rental, security costs) will be higher than necessary

The risk of spoilage and stock shrinkage will be increased, leading to increased costs

Similarly, holding too little stock is risky

A business may run out of stock, resulting in production stoppages and higher unit costs related to underused capacity

A sudden increase in demand may not be capable of being met and this leads to a loss of potential sales revenue

Just in time (JIT) stock management

Just in Time (JIT) stock management is a process in which raw materials are not stored onsite

Stock is ordered as required, and delivered by suppliers 'just in time' for production

Careful coordination is needed to ensure that raw materials and components are delivered by suppliers at the moment that they are to be used

Advantages and disadvantages of just-in-time stock management

Advantages | Disadvantages |

|---|---|

|

|

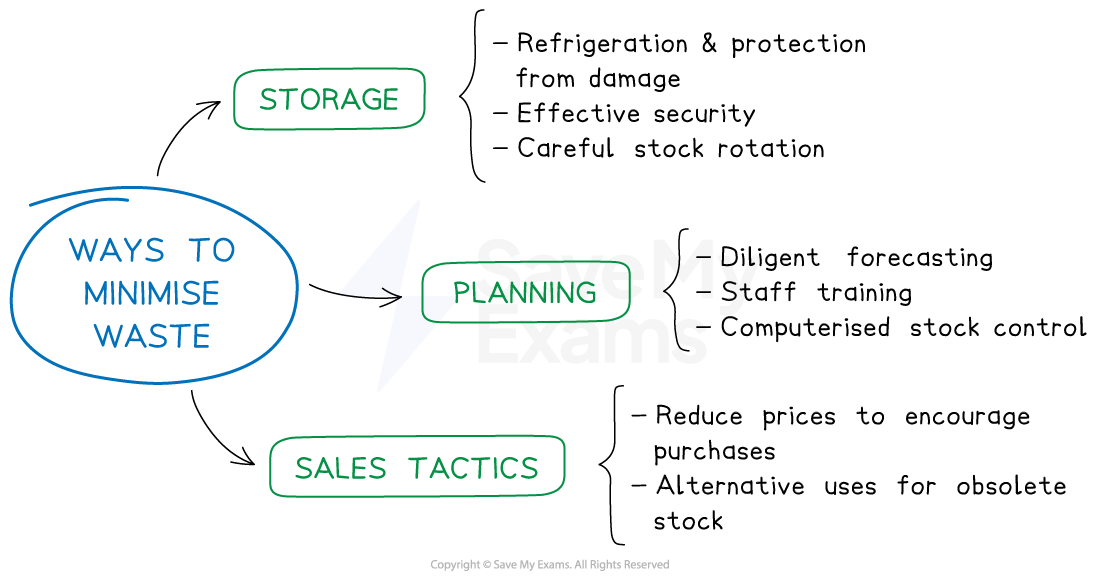

Waste minimisation

Waste in a business can occur for a number of reasons

Stock becomes obsolete unless used by a particular date

Perishable stock (food and medicines) that is not used before they deteriorate will need to be thrown away

Stock may be damaged as a result of poor storage conditions and may not be suitable for use in the production process

Allowing waste to go unchecked will increase the unit costs of production and reduce both efficiency and productivity

Businesses may take a range of steps to minimise waste

Ways to minimise waste

The minimisation of waste will depend upon the nature of the product

For perishable items, refrigeration and careful stock rotation can reduce waste

Staff training and computer inventory management systems may also reduce waste as fewer errors are likely to be made

Effective sales forecasting can help to reduce the amount of wasted stock

Competitive advantage from lean production

Lean production involves the minimisation of the resources used in production

Less time is required as the production process is organised in the most efficient way

Fewer materials are used as there is a focus on waste reduction

Less labour is used as lean production is typically capital intensive

The space required for production is reduced as a result of just in time stock management

A small number of trusted suppliers work closely with the business

The use of lean production is likely to lead to a competitive advantage

Lower unit costs are achieved due to minimal wastage, so prices may be lower than those offered by competitors

Better quality of output is likely as a result of supplier reliability and carefully managed production processes

You've read 0 of your 5 free revision notes this week

Sign up now. It’s free!

Did this page help you?